Cayman Islands Investment Funds: The latest updates for managers in Asia

In this webinar, we go over the latest regulatory implications that might impact your next fund launch as well as the current trends our independent directors are seeing that might affect your portfolio.

Speakers:

Moderated by:

Hello, everyone, and thank you for joining us today on today’s webinar on Cayman Islands Investment Funds, and the latest updates for managers in Asia. I’ll pass you over to my colleague, Elaine Chow, in Hong Kong. Thank you, Elaine.

Thank you, everyone. Thank you for joining us for today’s webinar. My name is Elaine Chow, and I’m a director at Waystone, based in Hong Kong. Waystone is a leading provider of institutional governance, risk, and compliance services to the asset management industry. With over 25 years’ experience, Waystone is now supporting asset managers with more than a trillion U.S. dollars in AUM. Today, we are very happy to have two of my colleagues, Rebecca and Claris, speaking with us this morning. Both of them are based in our Cayman Island office and serving as independent directors to investment vehicles with a wide range of structures and strategies such as hedge fund structured products, private credit, and private equity funds, covering multiple jurisdictions, including Asia.

About Our Speakers

Rebecca Palmer – Independent Director at Waystone

Rebecca joined Waystone from one of the Big Four firms, where she was an audit director in the asset management practice, overseeing Cayman funds for a variety of global managers ranging from new launches, to multibillion-dollar managers. Rebecca was also part of the emerging manager platform, working closely with managers with different strategies looking to launch Cayman funds. Currently, Rebecca is also heavily involved in ESG governance. She has spoken on many panels about ESG governance.

Claris Ruwende – Independent Director at Waystone

Our second speaker, Claris, she previously worked at a Cayman Islands monetary authority as a chief analyst, where she led the security supervision division team in carrying out a full range of regulatory functions to ensure the compliance of the licensing in registrants. Claris brings with her extensive experience in offshore financial services, and a strong working knowledge of the regulatory environment impacting hedge funds and securities investment business in the Cayman Islands.

Today, we will try to keep this webinar short, around 30 minutes. We will first give an update on the Cayman funds industry, and an overview of Cayman fund regimes and vehicles. We will then cover the regulatory and compliance requirements including AML/CFT, CRS and FATCA, and Cayman Economic Substance, as well as the Administrative Funds regime. Lastly, we will quickly touch on some other industry developments in Cayman Islands, and answer any questions you may have

Updates on the Cayman Fund Industry

So, Rebecca, over to you to start with giving a quick update on the Cayman fund industry, and an overview of Cayman fund regimes and vehicles. Thanks.

Thanks, Elaine. And good morning, everyone, and thank you so much for joining us. So, I thought it might be helpful, maybe, just to quickly give an update in Cayman Island, where we are in terms of the pandemic. So, we’re very fortunate. We’ve got over 80% of our population currently vaccinated, and in light of this, our borders reopened in November last year. The government announced last week that day two, five, and seven testing for travelers has been abolished, while so quarantine requirements remain in place for unvaccinated, but children of vaccinated adults take the vaccination status of their parents. So, it’s been fabulous to see tourists returning to the islands, as that sector has been hit hard by the pandemic. The digital nomad visa that Cayman introduced during the pandemic has attracted a number of high net worth individuals and family offices to relocate to the island, and has also seen new businesses set up on the island, and a number in the digital asset space, whilst the financial services sector has continued to strengthen during this time.

Increases in Regulated Funds

As of December 2021, there were 27,398 regulated funds, compared to 24,591 the previous year. The increase included a rapid growth in the number of regulated mutual private funds of 6.9% and 15.6%, respectively, and I think we’re particularly pleased to see that increase in private funds, following some of the legislation that was enacted in 2020. The last couple of years, as you’ve known, have seen an increase in legislation and an increase in enforcement action in response to some of the FATF findings, which my colleague Claris will cover in more detail later on, and there has been the fear by some that this would lead to the jurisdiction being viewed less favorably. However, this has not been the case, and the vast majority of managers understand the increased global regulation around AML and KYC and many of the regulatory enhancements as necessary.

Cayman has a very robust framework, and other offshore jurisdictions are now following suit, and adopting similar legislation. 2022 marks the 25th anniversary of the Cayman Islands Monetary Authority. CIMA continues to be a very approachable, pragmatic, and innovative regulator. Despite some of the regulatory changes, the managers we work with still speak very favorably with respect to the lack of red tape and getting set up and operational in Cayman, compared to some of the other jurisdictions they work in. We are very fortunate to have a highly-skilled workforce, world-leading service providers, political and economic stability, and an abundance of expertise in the investment funds, which continue to ensure that Cayman remains a leading financial services jurisdiction.

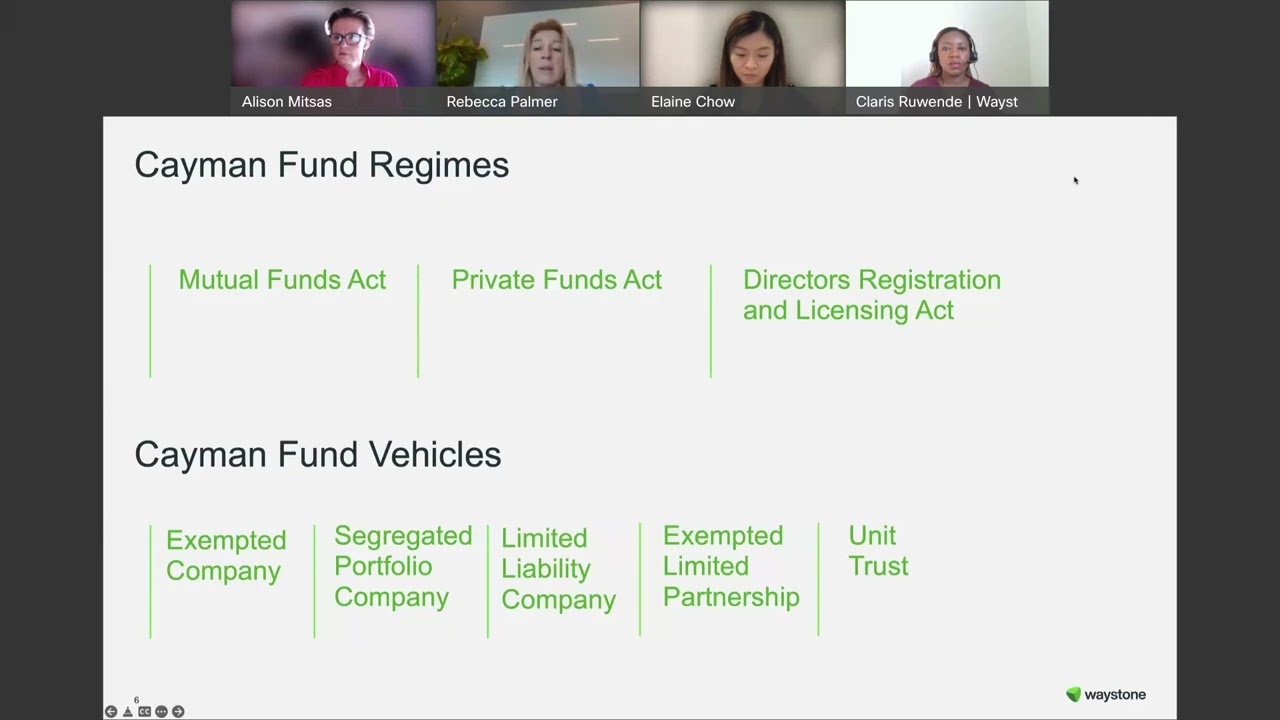

Common Cayman Fund Vehicles

So, just perhaps running through some of the common Cayman fund vehicles that you’ll see. Exempt companies and segregate portfolio companies are commonly used as open-ended funds, whilst closed-ended funds are typically structured as exempt limited partnerships. Limited liability companies are a relatively recent innovation, ideal for parallel funds that wish to replicate the terms of a U.S. LLC. Unit trusts are primarily used for investors in particular jurisdictions where other types of vehicles suffer tax or regulatory disadvantages. Cayman Islands investment funds are generally regulated by CIMA, under the Mutual Funds Act if they are open-ended, which would include most hedge funds, or Private Funds Act if they’re closed-ended, which would include most private equity, venture capital, real estate, infrastructure, and other funds investing in liquid assets. The exceptions to this rule include single investor vehicles, proprietary investment vehicles, and pension funds.

The Four Categories of Regulation

There are four categories of regulation to the Mutual Funds Act: licensed mutual funds, administered mutual funds, registered mutual funds, and limited investor mutual funds.

1. Licensed Mutual Funds

Licensed mutual funds are subject to full regulation by CIMA, and are largely confined to funds marketed locally in Cayman, and funds that comply with regulations done specifically for the Japanese retail market.

2. Administered Mutual Funds

Administered mutual funds are similar to licensed funds, except that a licensed Cayman Island mutual fund administrator must provide the fund with its principal office, and certify to CIMA that it believes the funds promoted to be of sound reputation, and that the fund will be properly managed and administered.

Registered Mutual Funds

Registered mutual funds are by far the most popular type of regulated mutual fund, comprising around 97% of all such funds. To qualify as a registered mutual fund, a fund must require a minimum initial investment of at least U.S. $100,000 or its equivalent in any other country, will have its interest listed on an appraised stock exchange. It’s still relatively straightforward to register as a mutual fund, with a registration certificate typically being issued within two to four weeks upon submission of the required documents. A corporate fund must ensure its directors are registered with CIMA under the Director’s Registration and Licensing Act, prior to the fund submitting its registration application. Each director must register with CIMA, using the CIMA portal. If the fund is a limited partnership, the directors and its general partner are not required to register separately, but certain identifying information must be submitted along with the registration application.

Limited Investor Mutual Funds

With respect to the limited investor mutual funds, previously, funds with less than 15 investors were not required to register with CIMA, so this was one of the big changes that came in a couple of years ago. And following the amendment to the mutual funds laws, these funds have been required to register with CIMA since August 2020. These funds are similar to registered mutual funds, except that they have no minimum investment requirement, the trade-off being that the fund cannot admit more than 15 investors, and the investors must have the right to appoint and remove the fund’s directors, general partners, or trustees as applicable by majority vote.

What are Master Funds?

A master fund is defined in the Mutual Funds Act as a mutual fund that has one or more regulated mutual funds acting as its feeder fund, which holds investments, and conducts trading activities to implement the feeder fund’s investment strategy. Master funds are required to register with CIMA as a subcategory of a registered mutual fund. And as some of you will be aware, CIMA also issued the rule of contents on offering documents, so we’ve seen a number of the managers we work with going through the process of updating their documents. There are various requirements here, and this is one of the key changes or key clarifications, so around including evaluation methodology, and including the powers to enter into within the document. So, I suspect a number of you have discussed this with your legal counsel.

Segregation & NAV Calculation Rules

Claris and I also spent a lot of time last year with our managers, discussing the segregation rules, and the NAV Calculation rule. And just to give a little bit of a refresher on those rules.

Segregation Rules

The segregation rules require that a regulated mutual fund appoint a service provided with regard to ensuring the safekeeping of the fund’s portfolio, for example, administrator custodian or investment manager. It is, however, not a requirement to engage a third-party service provider with respect to this function, and the operator could perform that role. The segregation rules require that a regulated mutual funds portfolio be segregated and accounted for separately from the assets of any service provider. It also requires that the fund ensures that none of its service providers use the fund’s portfolio to finance their own or other operations. There are, however, certain circumstances, for example rehypothecation, that are exempt from this requirement.

CIMA also issued a notice confirming the commingling of client assets in a context of a custody or sub-custody arrangement in accordance with established and accepted industry practice is not prohibited by the segregation rules. The segregation rules also require a mutual fund to establish, implement and maintain policies and procedures to ensure compliance with the segregation rules, and to ensure verification that the fund holds title to its assets, and record of the fund’s assets. This verification function is typically undertaken by a regulated mutual funds administrator and auditor, but the funds manager or operator may also perform the verification fund administering, subject to the function being carried out independently from the portfolio management function, and any conflicts being properly identified, managed and disclosed to investors.

NAV Calculation Rules

And so, with respect to the NAV Calculation rules, these require the regulated mutual funds to have in place a net asset value calculation policy that ensures that the funds NAV is fair, reliable, of high quality, and verifiable. The NAV Calculation policy should be in accordance with the applicable accounting standards that are used to prepare the financial statements. The fund’s NAV is required to be calculated by a service provided independent of the fund’s investment manager or operators, although the investment manager may be involved in the calculation of NAV, provided that this is disclosed in the funds offering documents. There is also a requirement to disclose any conflicts of interest caused by the investment manager’s involvement in the NAV calculation process. So for example, if the manager, you had [inaudible 00:11:20] value level-three assets, and manager was providing that price, that would need to be disclosed.

In addition to these rules, as part of these rules, the operator must approve and review at least annually the funds NAV calculation policy, and any pricing models adopted. So again, this is something that we would typically have as a standard item on our board meeting agendas, to ensure that we are reviewing and approving these. The NAV Calculation rule specifies a number of points the NAV Calculation policy must cover, but the most common one that we typically see missed is the requirement to include a practical escalation resolution procedure for the management of exceptions. So, say for example there was a NAV error, how would that be dealt with.

Ongoing Obligations for Mutual Funds

In terms of the ongoing obligations for mutual funds, mutual funds are required to pay an annual registration fee to CIMA by 15th of January, so hopefully, those of you with CIMA-regulated mutual funds have paid that fee. You are required to file your audited financial statements with CIMA within six months of the financial year end. Also, you’re required to notify CIMA within 21 days of becoming aware of any change that materially affects the information in the current offering document. As discussed, you’re also required to keep the fund’s assets segregated, and accounted for separately from the assets of any other person. And they’re also required to comply with the AML regulations, which Claris will kindly take us through in more detail later, as well as complying with FATCA and CRS notifications.

The Private Funds Act

The Private Funds Act, so moving on now, this excludes non-fund arrangements listed in the schedule, such as proprietary vehicles and securitization vehicles, joint ventures, and holding vehicles. I think for a number of our managers that we work with, it was quite a lengthy exercise to determine which funds needed to be registered with CIMA, and a number of managers engaged legal counsel to assist with this process when this legislation first came in. A private fund is required to register with CIMA within 21 days of admitting any new investors…sorry, any investors, and in any event prior to accepting any capital contributions from investors. Registration for private funds is very similar to that of a mutual fund in terms of the application process, and again, registration will be effective from the date the application is filed, but confirmation of registration may take two to four weeks to receive. In terms of the ongoing regulatory obligations, again, it’s very similar to that of the mutual funds, you know, in terms of fees being due, to be paid by January 15th, the financial statements needing to be filed within six months of the year end, however, there are additional operating requirements relating to valuations, title verification, and cash monitoring.

So, these valuation requirements, private funds must adopt appropriate and consistent procedures for proper valuation of assets, with valuations being carried out at least annually in accordance with accounting standards adopted by the fund.

Again, this is an area where we’ve been speaking with a number of managers, some managers might naturally have preferred to keep certain investments at cost, but the accounting frameworks require that these are measured at the fair value. These valuations must be carried out by the fund administrator, or another appropriately qualified independent third party, or the funds manager or operator, provided that the valuation function is independent of the portfolio management function, and potential conflicts are disclosed, and the fund’s written valuation policy, including details of the person responsible for evaluations, must be disclosed to investors. So again, when we’ve been seeing some of the updates to the offering documents, we’ve been seeing the valuation policy included in that, or alternatively, including a reference that it is available upon request.

Title Verification

With respect to title verification, private funds are required to appoint a custodian for their assets, except when it is neither practical or proportionate to do so. In practice this is often the case, except where a private fund is trading publicly listed securities. With respect to cash monitoring, private funds must appoint a person to monitor cash flows, ensure cash has been booked in the appropriate cash accounts, and ensure all payments made to investors have been received. With respect to private fund marketing materials, neither the Private Funds Act nor CIMA currently requires a private fund to have an offering document or marketing materials, but if a private fund does issue any marketing materials to solicit subscriptions from investors, these must be filed with CIMA, and comply with the contents rule that we just covered, with respect to mutual funds.

Fund Directors Registration & Licensing Act

And I’m just briefly going to cover the Directors Registration and Licensing Act. So, directors of covered entities are divided into three categories:

1. Registered Directors

The first being registered directors. So, a registered director is a natural person appointed as a director of fewer than 20 covered entities, and is required to be a registered director. You know, they are not regulated by CIMA. The fees for becoming a registered director are $8,530, so relatively affordable. And with respect to this, what you’ll probably find is that most of you are sitting…you know, as investment managers, if you’re also sitting on your Cayman fund’s boards, provided that you have less than 20 entities, you will be sitting in this registered director category.

2. Professional Directors

And for directors like myself and Claris, we’re in the second bucket, which is professional directors. Professional directors are defined as natural persons appointed as directors for 20 or more covered entities, and we are…you know, we have to submit a formal license application, and once successful, we are regulated by CIMA.

3. Corporate Directors

And the third category is corporate directors, which is a body corporate appointed to act as a director.

Ongoing Obligations for Fund Directors

The ongoing obligations for directors include professional directors and corporate directors must maintain a minimum of CI $1 million in insurance coverage. That being said, litigation is very expensive, so we would generally encourage at least $5 to $10 million in DNO coverage being purchased. You are required to pay the annual fee to CIMA to maintain your registration, and such fees are also due by the 15th of January. And if you are late paying those, there is a penalty of 1/12 of the annual fee for each month that it’s late. You are also required to file a notice of any change to the information supplied in the registration licensing application within 21 days of that change taking effect, and it’s really important that you do so. So, say for example you take on a new fund appointment, or something in your personal details changes, you do need to update the CIMA portal for those, because there are some serious penalties for failing to comply with that requirement.

So, I appreciate there’s a lot of information I’ve covered in this one slide, so I will stop there, and hand over to Claris.

Great. Thank you, Rebecca. Thank you for that update. Very timely. So, I know there is no update of Cayman funds environment that does not involve a regulatory filing piece, so in this section, we’re just going to talk about those filing requirements, what has been happening in the AML/CFT space, what is it that you have to look out for as fund managers. So, we’ll start here, with the AML/CFT/CPF updates.

AML/CFT/CPF Updates

As you know, the Cayman Islands has really focused on this area in the last few years, particularly driven by the mutual evaluation report that was issued in March 2019 by the Caribbean Financial Action Task Force, as Rebecca previously mentioned. In 2021, they then sent out a follow up report for the Cayman Islands, which really, you know, explained that there was 60 out of 63 recommendations that Cayman Island’s legal framework was in compliance with, but there was those three that were pending. And so because of that, we are, as a jurisdiction in the Cayman Islands, under increased monitoring by the Financial Action Task Force. So as you know, in the last few years, in response to this, the Cayman Islands monitoring authority, as well as the Cayman Islands government has been working to try and make sure we get into compliance with the requirements of the Financial Action Task Force so that we can be removed from this increased monitoring, or grey list.

Technical Compliance Requirements

An update there as well, aside from the 63 recommendations by the Financial Action Task Force, there is also technical compliance, and of those, there is 40 technical compliance requirements. So, what are these? This is where the Financial Action Task Force is trying to look to see if we actually have the regulatory laws in place to be technically compliant with what the laws are required around AML/CFT. So, it’s a good number there that Cayman had, where we had 39 of those areas sufficiently covered, and in Q3 of last year, we found out that we are now compliant with all 40 areas. So, that’s quite a strong demonstration of the regulatory framework in the Cayman Islands, and we’re quite proud of it. And, you know, all parties are working quite…to make sure that by Q3 of 2022, we at least are considered to be removed from the Financial Action Task Force.

And so, because of this enhanced monitoring from the Financial Action Task Force, there has been quite a lot of changes in the Cayman Islands AML jurisdiction, AML requirements. As you can see on these next two slides, there’s a few changes that we have listed in there of what has changed in terms of AML regulations, as well as the guidance notes.

Key Changes in AML Regulations

So, key changes that we would want to highlight here is the change to the equivalent jurisdiction list for country risk assessments, as well as the beneficial ownership threshold, where the beneficial ownership threshold has been set to 10%. And then for eligible introducers as well, where there’s certain information that’s required, where you have relied on eligible introducers to be maintained. So, there’s quite a few changes, which you can look at once we’ve circulated these slides, and have a better understanding of whether or not you have stayed in compliance with those changes.

Appointing an AML Officer to Act as AMLCO

I want to highlight two slides down, Ali. The requirement for AML officers, which is a key thing that you have to make sure that all our funds, and any other licensed entities have appointed a natural person as an AML officer to act as AMLCO, and money laundering reporting officer as well. There’s a few requirements there for what these officers need to do, but the key one that we would want to highlight at this point is that these officers need to be autonomous, and they need to have sufficient time to execute these duties. So again, I’ll speak here and say Waystone does offer these services, where you can appoint one of our natural persons that can act as AMLCO, MLRO or DMLRO to be in compliance with this regulation. And of course, these names have to be submitted to CIMA so that they are aware who are the people who are working in this function.

Increased Focus on AML/CFT Inspections

And again, because the Cayman Islands has a strong regulatory framework, and they’re trying to demonstrate this, there has been an increased focus on AML/CFT inspections in the jurisdiction. Now, I’ll highlight here that for funds, these types of inspections are conducted on new administrators or the AML delegate, because they are the ones conducting the function of onboarding investors. However, for Securities Investment Business Act registered persons, which we’ll call them SIBA RPs going forward, these inspections are quite direct on your operations as a manager of the CIMA registered SIBA RP. And the inspections that have carried on in the Cayman Islands in the last year or two, we had an industry update from CIMA, where they sort of highlighted the key areas where people were defaulting, and again, we have sort of given you a summary here to, you know, give an indicator of the areas where people are falling short.

And one thing to highlight with the CIMA inspections for AML/CFT also is that they are full scope AML/CFT, which means they would cover areas like corporate governance, outsourcing, internal controls, as well as the AML, you know, pieces themselves. So in terms of corporate governance, as you can see, mostly the issue was there was no minutes, or there were conflicts of interests, for example, where the money laundering reporting officer is also director of the entity. This is a key one that keeps recurring. So again, another mention there to say if you’re going to appoint an MLRO, they have to be autonomous, and they have to be independent. And then on the outsourcing, it’s just to make sure there’s actually outsourcing policies and procedures, and that there is an agreement in place, and there’s also measurement of performance of those service providers.

AML-Specific Findings

And then in the next slide, please, Alli, is a list of all the AML-specific findings, right, where the authority wanted to highlight here the importance of sanctions screening. Because in most of the cases, they were finding that providers are not including Cayman sanctions lists in their scrubbing, and that’s probably required. And another key gap was where group-wide AML policies are being followed, there wasn’t a gap analysis to bring those AML requirements to align to Cayman Island-specific legislation. So again, this is just to give you an update of what’s been happening in the regulatory space, so that you’re well aware.

FATCA & CRS

And we’ll move on to the next slide now, and speak about FATCA and CRS. This area, again, is more for the investors into the funds, and so there’s a requirement there for USA investors to comply with FATCA, and then for all the CRS participating jurisdictions to comply with CRS reporting. In terms of deadlines, just to re-highlight those, FATCA and CRS returns are due by the 31st of July, of 2022. So if you’re working on that, just have that date in mind. And then there is also the CRS compliance forms, which are covered in the next slide, and those are due on the 15th of September, 2022. So, those are just some key dates to keep in mind on the FATCA and CRS space. And if you’re a new manager trying to form your structures and your funds, just to be mindful that you want to have this in mind, and think of who is going to be your AUI delegate to take care of this function, to make sure the investor reporting is done correctly for this. All right, so we won’t dwell too much on the FATCA and CRS, and we will move on to economic substance.

Now, this is a new law, again, that came through in 2019, where the Cayman Islands, in response to the global standards established by the EU, has implemented this to be in compliance with all their requirements for OECD Base Erosion and Profit Shifting. Now, what this law requires, basically, is that all relevant entities that are conducting relevant activities and earning relevant income must satisfy a three-criteria economic test in relation to that. Now, this particular portion, again, does not directly impact our fund space, because the funds are exempt. So for the funds, as long as you file your economic substance notification in a year, you are compliant with your requirements. However, again, for the SIBA RPs that we mentioned earlier, there is a further requirement here that if you do the business of fund management, then that is a relevant activity, and you are in scope for reporting.

Now, the key thing with the three-criteria economic test is that managers should be able to demonstrate that they’ve been directed and managed from the Cayman Islands, and that they’re conducting certain core income-generating activity from the Cayman Islands, and also that there is proportionality of the expenditure and fiscal presence in Cayman, compared to the revenue that’s being generated. Now, in the core income-generating activity, this would be things like portfolio management for fund managers, this would be risk reporting, this would be regulatory reporting, or investor reporting as well.

Penalties for Lack of Compliance

Next slide, please, Ali. And in this slide, again, it just further elaborates the relevance of this, where it is stated that there is penalties for lack of compliance, or for lack of being able to demonstrate that there is economic substance here in the Cayman Islands, and the first year will be $12,500, which would increase significantly to $125,000 in the second year. And again, as mentioned before, funds have to put in their notification, all entities have to put in their notification, only for funds, it would state that they’re not in scope, and for the SIBA RPs, it would state that they’re in scope, and that a return has to be filed 12 months after that financial year end. The key highlight here is that there has been an update to the law now, and it now includes general partnerships, limited partnerships, exempted limited partnerships, and foreign limited partnerships as well, that are now required to also submit ESNs on an annual basis. When the law was rolled out originally, these entities were not in scope. And then some key dates there, again, which you can refer to for your own reminding for the filings that have to be done.

Enforcement & Supervisory Actions

Next slide, please, Ali. Right, and because of all the changes, like we said, the regulatory focus, remember, we spoke about the FATF, and having 60 out of 63 recommendations that we as a jurisdiction had complied with. The other three that remain were mostly around enforcement and supervisory actions being taken here in the Cayman Islands against people that default. So as a result, naturally, the Cayman Islands has enhanced its administrative fines regime, as covered in the next few slides as well. As you can see, there’s quite some hefty fines there, starting from minor breaches that are around $6,000, and very serious breaches that can take you up to $1.2 million in terms of admin fines. And we have also taken the time to just give you a breakdown, or at least key highlights of what would be a minor breach, what would be a serious breach, what would be a very serious breach, so the next two slides will show you that breakdown. And again, we will share these slides, and you will be able to go in more detail. But as you can see, something that’s a minor breach is just basically not paying the annual fees that Rebecca mentioned earlier, when it’s due. That consists a minor breach, and could set you off $6,000. And then there’s serious breaches, such as not appointing an AML officer. As we’ve highlighted, that’s a key requirement as well, or notifying of any changes to CIMA.

And on the very serious breach list is things like non-compliance to Cayman Islands authority requests for information, which is the next slide. Thank you, Ali. As you can see here, so if the supervisory authority reaches out to you for requirement of documents, and you’re not able to provide them in the time, that can be classified as a very serious breach. And also there to highlight, the point on Private Funds Act, that the non-compliance of an operator with those Private Funds Act requirements can constitute a very serious breach, and can set you off another $1 million dollars.

So, that brings me to the end of the short overview that we had on the regulatory space in the Cayman Islands, and what the requirements are there. So, I’ll hand over back to Elaine, I guess, at this point, so that you can direct us for this call. Thank you.

ESG Governance in Cayman

Thank you. Thanks, Claris. I think before we end today’s webinar, I’m not sure if there’s any other industry update that you would like to share. Perhaps, Rebecca, you might also want to quickly touch on the ESG governance in Cayman, since I know you’re heavily involved in the ESG governance. Is there anything you would like to share with our audience today, maybe just a quick look?

Yeah, just very briefly, obviously ESG and responsible investing is a hot topic. We’re having a number of conversations with our managers, who are being asked about this by their investors. Internally here in Cayman, there are a few committees that are discussing what we should do from a regulatory standpoint. You know, we are a small island, we are very, very susceptible to climate change here, so it is something we really do care about as a jurisdiction, and as any manager will have seen, there’s been a lot of legislation coming out of the European Union. We expect to see some more in the U.S. And obviously, Cayman is sort of in the middle of those two jurisdictions, so I think we will be moving, potentially, to see a bit more regulation here in Cayman around that. But it’s yet to be determined at this point, but something, certainly, that we’re actively involved, as Waystone, in those discussions.

Thanks, Rebecca. I think that was really helpful. I think we’re almost running out of time, so we will address your questions after the webinar, and we will circulate the slides. If you have any questions, or require any assistance of Cayman regulatory and compliance matters, please feel free to reach out to any of us. We are more than happy to have a conversation with you. Thanks again for joining today, and I hope you all found the webinar helpful. I wish you all a good day. Thank you.